Exam for new fair value credential is now available

After several years of hard work by the AICPA, ASA, and RICS, the exam for the new valuation credential, the Certified in Entity and Intangible Valuations™ (CEIV™), is now available to professionals involved in fair value for financial reporting.

Do you qualify? If you have a business valuation credential from the ASA, AICPA, or RICS, you need to meet the experience and education requirements specific to fair value and the CEIV credential. You need 3,000 hours of fair value experience over the past five years and take a two-part course and pass the two-part exam. The first part of the course is a body of knowledge on general accounting and valuation issues related to financial reporting, and the second part is education related to the Mandatory Performance Framework (MPF), which is a set of best practices all CEIV holders must follow. The exam is also in two parts that correspond to the education, and each part contains 60 questions and will take two hours to complete.

The AICPA, ASA, and RICS offer the credential, and they all offer online and live training. The exam is a timed online exam that is the same no matter which organization administers it. For more information, a special website has been set up for the credential.

BVR presented a recent webinar, CEIV: Ready, Set, Go!, that explains the credential and how to get it. William Johnston (Empire Valuation Consultants LLC), chair of the ASA’s BV committee and the ASA’s CEIV program development representative, conducted the webinar.

Draft expert reports may be vulnerable to discovery

Experts may have heard that the federal discovery Rule 26 protects draft reports from discovery. But a side ruling in a recently reported patent infringement case makes clear this rule is negotiable. The lesson is that, if you want to limit the risk of exposure, use the phone or web technology to discuss your draft.

Adulterated vs. unadulterated draft: The defendants in a patent infringement case revolving around snowmobile technology asked the court to order the plaintiffs to produce draft reports that were exchanged between two of the plaintiffs’ technical experts. As it turned out, one expert had sent his draft to the other expert, and vice versa, for review and comments. As one expert explained in his deposition: “Rarely do I ever view a report and not have at least … some suggestion on it.” The exchange was part of what he called “the quality assurance process” that took place before the experts finalized their respective reports.

Federal Rule of Civil Procedure 26(b)(4)(B) protects “drafts of any report or disclosure … regardless of the form in which the draft is recorded.” The court in the instant case acknowledged that a pretrial order stated that drafts of expert reports generally were not discoverable. But, said the court, at issue was not “an unadulterated expert report draft copy” but draft reports with editorial comments from a different expert. According to the court, considering Rule 26(a)(2)(B)(ii) provides for disclosure of “all the facts and data” another party’s expert has considered in forming his or her expert opinion, the defendants were entitled to see the comments on the contested drafts and, for context, also the portions of the drafts to which the comments related.

The case is Bombardier Rec. Prods. v. Arctic Cat Inc., 2016 U.S. Dist. LEXIS 184531 (April 19, 2016). A digest discussing the discovery ruling and the related patent ruling is available at BVLaw.

New study illustrates need to mix valuation with forensics

Valuation and forensics often go hand-in-hand, and the latest report from the Association of Certified Fraud Examiners (ACFE) illustrates this. Companies lose approximately 5% of revenues to internal theft and financial misstatement each year, and it can have a big effect on valuation.

Valuation impact: Fraud affects revenue and cash flow and can also have an effect on the company’s reputation and goodwill. When looking at pricing multiples keyed to revenue, the impact of fraud can cause a valuation to drop materially. Using the 5% figure from the study, if a pricing multiple of 1.5 times revenue is used, this means a value impairment of 7.5% (5% times 1.5).

The notion that small companies are riskier than larger companies generally holds true regarding fraud. The 2016 ACFE study revealed that check tampering, skimming, payroll, and cash larceny schemes were twice as common in small organizations as in larger ones. However, corruption was more prevalent in larger organizations. Industry also affects the fraud risk assessment, according to the report, with banking and financial services, government and public administration, and manufacturing as the sectors most likely to experience fraud.

What to do: Do a fraud risk and assessment and customize it depending on the size and industry of the subject company. This includes an evaluation of the firm’s internal controls, such as looking at formal policies and procedures and any mechanisms in place, including reporting hotlines or anti-fraud training. Also, when interviewing management, ask about any past incidents of fraud and try to get a sense of whether the corporate culture has any effect on the possibility of fraud. For example, are managers under severe pressure to meet budget or sales goals? If your probe indicates a hotbed of fraud, you may have to bring in a financial forensics expert. For the future, beef up your own abilities by adding an understanding of forensic tools to your valuation arsenal.

The use of restricted stock studies is the most cited methodology for quantifying a discount for lack of marketability (DLOM). A 2016 BVR survey revealed that 76% of respondents say they use restricted stock studies and over half (56%) say they use the FMV Restricted Stock Study™.

Filter transactions by profitability measures, revenue, block size, book value, total assets, and more;

Access up to 60 data fields per transaction;

Stay current with new, thoroughly updated transactions added quarterly;

Convert discounts from one-year and six-month holding period transactions to a two-year equivalent holding period; and

Access the Stout DLOM Calculator to simplify their process by creating exhibits and worksheets that can be inserted into valuation reports and be used to make their conclusion even more defensible.

Pratt’s Stats now lists over 26,500 private-company M&A transactions thanks to business brokers and other intermediaries who contribute the data. Individuals who send in the most transactions are inducted into the Pratt’s Stats Hall of Fame. For the first quarter of 2017, they are:

Chris George, George & Co. (Worcester, Mass.);

Al Statz, Exit Strategies Group Inc. (Petaluma, Calif.); and

Trevin Rasmussen, Bristol Group (Boise, Idaho).

BVR wishes to thank to these individuals and all of the other brokers who help maintain Pratt’s Stats as the most reliable data source of its kind.

Timely topics, top-notch speakers at ASA’s fair value event in Los Angeles June 1

Last year, BVWire attended this event, and it was excellent—and this year’s program offers another must-attend conference for anyone involved in fair value. It’s the ASA/USC 12th Annual Fair Value Conference in Los Angeles on June 1. One exciting session will be a Fair Value Auditor panel where the new Mandatory Performance Framework is intended to be the key area of discussion. Tony Aaron, formerly with Ernst & Young andwho is now on the faculty at USC Leventhal School of Accounting, will be the moderator.

Another interesting session will be one on valuation dilution with Amanda Miller (Ernst & Young). “This is a topic that’s often overlooked but it impacts many business valuations where future financing rounds or significant option grants are expected,” says Ray Rath (Globalview Advisors), one of the event’s organizers. He tells BVWire that this topic has a strong impact on early-stage company valuation for ASC 718 and ASC 946 (venture capital fund reporting).

Particularly timely is a session on contingent consideration—there will be a panel discussion that includes two members of The Appraisal Foundation task force that developed the exposure draft on the topic.

Check out the entire agenda, and we hope to see you there!

A leading firm in business valuation and litigation support, Meyers, Harrison & Pia (MHP) has merged with Marcum LLP, a national accounting and advisory services firm. MHP brings to Marcum 55 partners and staff located in New Haven, Conn., and Portland, Maine. Marcum, based in New York, ranked 16th on Accounting Today’s list of the “Top 100 Firms,” with $449 million in annual revenue.

MHP is a full-service CPA firm providing accounting, audit, tax, and advisory services to a wide range of clients and industries. The firm specializes in complex business valuation, financial forensic, and litigation support engagements. MHP partners serve frequently as expert witnesses, and they are authoritative speakers, authors, and reviewers on valuation and economic damages topics. For example, MHP’s Nancy Fannon is the co-editor (with Jonathan Dunitz) of The Comprehensive Guide to Economic Damages, 4th edition, and is the co-author (with Keith Sellers) of Taxes and Value: The Ongoing Research and Analysis Relating to the S Corporation Valuation Puzzle.

"Joining Marcum will give MHP's clients and staff significantly greater resources as well as access to a deep bench of talent across the firm's practice areas, including in advisory services,” said MHP CEO Mark Harrison in a release.“Our combined expertise constitutes one of the strongest valuation and litigation support practices in the country." Harrison will join the Marcum Executive Committee. The MHP entities that merged with Marcum are Meyers, Harrison & Pia LLC and Meyers, Harrison & Pia Valuation and Litigation Support LLC.

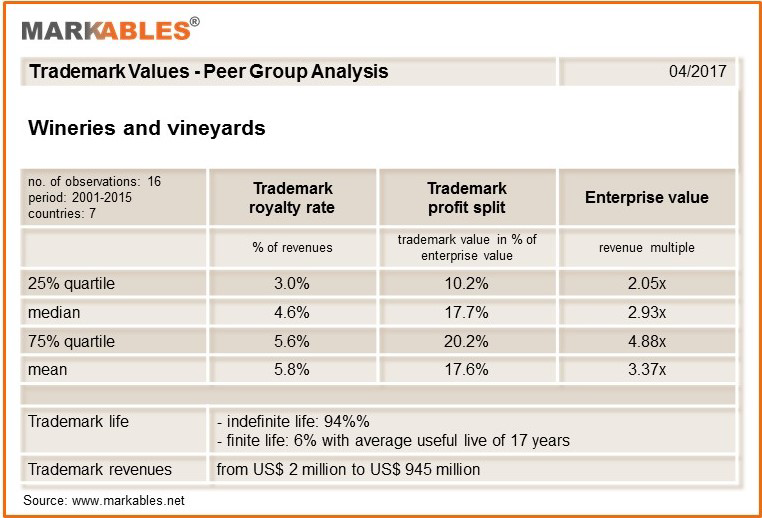

Vineyards and wineries do not face easy circumstances to build strong brands. For example, product quality may be subject to changes, and these businesses often cannot simply expand their capacity. Still, branding is important in the wine sector, which is the subject of this month’s sector snapshot from MARKABLES, a Switzerland firm that has a database of over 9,000 global trademark valuations published in financial reporting documents of listed companies. It analyzed the brand in the purchase price allocations of 16 different wine businesses acquired between 2001 and 2015 (see table). The businesses are located in seven countries and have revenues from $2 million to $945 million. The peer group includes brands such as Penfolds, Jackson-Triggs, Hardys, Robert Mondavi, Clos du Bois, Fetzer, and Meiomi, to name a few.

Because of the high value of tangible assets (vineyards, vines, cellars, and stock), wine businesses enjoy high valuations of 3x revenues on average. The brand is the single most important intangible asset, accounting for 17.5% of enterprise value on average. Wine brands are typically assumed to have an indefinite life and a mean royalty rate of 5% on revenues. This is higher than for coffee, pasta, and sports brands but less than nutraceuticals. However, as the retail price for a bottle of wine can go from less than $10 up to more than $1,000, there is a very wide range of brands—from commercial mass market wine brands to superpremium brands. Therefore, the range of observable royalty rates for wine brands goes from 1.25% to 15%. Hopefully, the next vintage of your favorite wine brand will be century-old wine!

People: Rob Schlener was appointed assurance and advisory practice leader at SingerLewak in Los Angeles … Securities litigation specialist Therese Doherty has joined the New York City office of Mintz Levin.

Firms: Cherry Bekaert has announced the launch of a Technology Solutions Group, to be led in part by recently hired director Jim Holman, who will be based in the Atlanta office. The Group will operate from the firm’s Atlanta and Greenville, S.C., practices … Gerson Preston announced a relocation of its Boca Raton, Fla., office into an expanded space to accommodate anticipated future hires. As part of the lease terms, the accounting firm will possess naming rights to the building … Withum has expanded its array of digital services by acquiring IT consulting firm Portal Solutions and its two offices in Bethesda, Md., and Woburn, Mass.

Important note to webinar attendees: To ensure that you receive your dial-in instructions to BVR’s training events, please make sure to whitelist bvreducation@bvresources.com.

Your discussion could be featured here—BVR's LinkedIn group is a place for valuation professionals to share, discuss, and learn about compelling BV topics. If you're not already a member, request to join: