Judge Laro calls Section 1031 appraisal ‘tainted’ and ‘useless’

Attendees of the 2015 AICPA conference may remember a session in which David Laro, senior judge of the U.S Tax Court, cautioned against attorneys who seek to steer the valuation. If discovery reveals the attorney’s undue involvement in the valuation, the appraisal and the expert’s reputation may be damaged. A recent Section 1031 case that Judge Laro adjudicated shows he had a specific situation in mind.

Sale-leaseback strategy: The taxpayer wanted to minimize the tax consequences of a $1.6 billion gain resulting from the sale of two fossil fuel power plants. It decided to pursue a Section 1031 exchange that allows for the deferral of gain where the relinquished property is exchanged “solely for property of like kind which is to be held either for productive use in a trade or business or for investment.”

In a nutshell, the taxpayer used the untaxed proceeds from the sale to lease a number of like-kind replacement properties from tax-exempt third parties, in different states, for a term exceeding the plants’ useful life and then subleased them to the plants’ original owners. At the end of the subleases, the sub-lessees had a cancellation/purchase option.

A Chicago law firm provided tax advice, and a nationally known financial firm appraised the relinquished properties and the replacement properties. Because of its work on the sold properties, the appraiser knew how much gain the taxpayer wanted to defer.

The crux of the appraisal was that the fair market value of the replacement properties at the end of the leaseback term would be less than the cancellation or purchase-back option price. The replacement property owners would not be economically compelled to exercise the cancellation/purchase options. As such, the transactions represented a genuine equity investment on the taxpayer’s part rather than a financial arrangement.

The Internal Revenue Service disputed that the transactions met the Section 1031 requirements, and the taxpayer petitioned the Tax Court for review.

Flagrant letter: Discovery revealed that, as the appraiser worked on the appraisal reports, the lawyers provided continuous feedback. A flagrant attorney letter to the appraiser included a list of “appraisal conclusions we anticipate will be necessary to support our tax opinion issued in connection with any leasing transaction.” As Judge Laro noted, the list appeared “almost verbatim” in the appraisal reports.

The court agreed with the IRS expert who contended the appraisal had serious technical flaws. But the court seemed most disturbed by the attorneys’ conduct, which it said compromised “the integrity and independence of the appraisal process.” The law firm provided the conclusions “it expected to see in the appraisals to be able to issue tax opinions at the ‘will’ and ‘should’ level.” This degree of interference “improperly tainted the … appraisal, rendering it useless,” the court said. Moreover, it tainted the attorneys’ tax opinions.

The court decided the transactions failed to qualify as Section 1031 exchanges and the taxpayer was not entitled to the various deductions it had claimed related to the transactions. The court also ruled in favor of accuracy-related penalties. The taxpayer was sophisticated and claimed to have read the law firm’s tax opinions in their entirety, the court noted. Accordingly, it knew or should have known that the opinions were based on flawed appraisal reports. Relying on the opinions was “misguided,” the court said.

The case is Exelon Corp. v. Commissioner, 2016 U.S. Tax Ct. LEXIS 26, Sept. 19, 2016. A digest of the decision and the court’s opinion are available at BVLaw.

back to top

Samsung scores against Apple, but end result remains unclear

It’s still not over. A recent ruling from the U.S. Supreme Court does not end the long iPhone design dispute between Samsung and Apple, but it promises to cut down the huge damages Apple was awarded by a jury.

‘Article of manufacture’: After Apple released its original iPhone in 2007 Samsung came out with a series of smartphones that closely resembled the iPhone. Apple sued in 2011 alleging Samsung’s phones infringed three design patents. A jury agreed and awarded Apple $399 million in damages.

Samsung appealed to the Federal Circuit, arguing that considering a phone was a multicomponent product, the infringer should not have to pay for profits it made on the sale of the entire phone but only on the infringing parts, such as the screen or case. In other words, just as with utility patents, damages should be apportioned to the infringing component(s). The court disagreed, citing a 19th century statute that prohibits the unlicensed application of a “patented design … to any article of manufacturer for the purpose of sale” and makes the infringer liable for “the extent of his total profit, but not less than $250.” According to the Federal Circuit, “article of manufacture” meant the entire phone since the “innards” of Samsung’s phones could not be sold separately from the phones’ shells.

Samsung, supported by the tech industry, asked the Supreme Court for clarification on whether the term “article of manufacture” always means the end product sold to the consumer or whether it also can mean a component of that product. In a world of multicomponent products, only the latter interpretation makes sense, Samsung argued.

The Supreme Court noted the term “article of manufacture” as used in the statute included “both a product sold to a consumer and a component of that product.” The Federal Circuit’s interpretation was too narrow, the high court said. Whether or not the article was sold to the consumer separately was not the decisive factor.

But the court declined to create a test for identifying the relevant article of manufacture in a given situation. Instead, it sent the case back to the Federal Circuit to set forth a test and then apply it to the case for each of the three design patents.

Takeaway: Samsung won in that the Supreme Court agreed that it is not per se liable for profits derived from the sale of the entire phone, but Samsung still does not know how much its liability to Apple is.

The case is Samsung Elecs. Co. v. Apple Inc, 2016 U.S. LEXIS 7419, Dec. 6, 2016. A digest of the decision and the court’s opinion will be available soon at BVLaw.

back to top

Section 2704 cliffhanger

Now that the IRS hearing on the Section 2704 proposed regs is history (see coverage here), everyone is waiting to see what happens next. We do know, based on IRS remarks at the hearing, that the final regs will not include an “implied put right” and will make it clear that the three-year rule will not be retroactive. It remains to be seen, however, how the IRS will respond to comments about other issues, such as how the regs redefine long-accepted definitions of fair market value, marketability, and control.

The main VPOs—the AICPA, ASA, and NACVA—all sent representatives to testify. NACVA had the strongest showing, with three speakers taking the podium on its behalf: Peter Agrapides (Western Valuation Advisors), Robert J. Grossman (Grossman Yanak & Ford LLP), and Mark Hanson (Schenck SC). NACVA also did a post-hearing video that you can watch if you click here. You’ll also find links to NACVA’s testimony and a transcript of the entire hearing.

back to top

TAF issues third exposure draft of USPAP 2018-19

The Appraisal Foundation has announced that the Appraisal Standards Board (ASB) has issued the third exposure draft of proposed changes for the 2018-19 edition of the Uniform Standards of Professional Appraisal Practice. Some of the issues under consideration deal with the definition of report and communication of assignment results. There’s also a proposed revision of the definition of appraisal review, as well as splitting the existing Standard 3 into two standards. Written comments are requested by Jan. 27, 2017, and can be sent to ASBComments@appraisalfoundation.org.

back to top

Big 4 offer their outlooks on tax reform

The incoming Trump administration is preparing to push for the biggest tax overhaul in three decades now that Republicans dominate both houses of Congress as well as the executive branch. The Big 4 have issued reports providing an overview of the tax reform process that is now underway.

KPMG’s report says: “Although enactment of tax reform legislation in the near future is by no means certain, the odds for reform being enacted soon appear higher than they have been at any other time since the Tax Reform Act of 1986 became law.” Similar reports have also been issued by PwC, Deloitte and Ernst & Young.

back to top

Global BV News

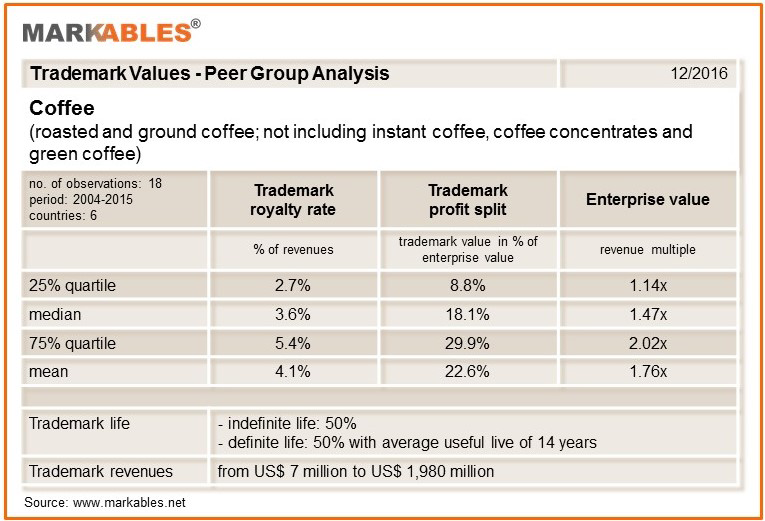

Coffee: It’s all about the brand

Coffee is a perfect example of how branding can add value to a business. Despite being a commodity with little room for differentiation in a mature market, branded coffee businesses show strong profitability and enterprise value. This is due to branding and the resulting consumer preferences it triggers. In blind testing, consumers taste differences between bean or roast varieties, but such differences are virtually nonexistent between brands. In such cases, it is the brand that makes the difference, not the product itself.

Good to the last drop: In an analysis of 18 global coffee brands acquired between 2004 and 2015, average royalty rates for coffee trademarks were between 3.5% and 4%, according to data from MARKABLES (see chart below). The trademarks of coffee businesses account for 20% of enterprise value, ranging from 10% to 30%. The average sales multiple paid for coffee businesses is between 1.5x and 1.75x revenues. The peer group includes brands like Folgers, Van Houtte, Douwe Egberts, Café Bustelo, Café Pinon, among others. Not bad for a product that is basically a commodity, and for peers that are mostly second- or third-tier players. Valuation multiples for the market’s leading brands would be even higher, but they are rarely subject to acquisition.

(click image to view full size)

MARKABLES (Switzerland) has a database of over 8,200 global trademark valuations published in financial reporting documents of listed companies.

back to top

|

January issue of Business Valuation Update debuts global coverage

Starting with the January 2017 issue of Business Valuation Update, you will see more articles with a global perspective. But don’t skip over an article contributed by someone not in your home country. Most of what they say will be relevant no matter where your practice is located. Here’s what you’ll see in the next issue:

- “30 Field-Tested Ideas to Bring in More BV Business” (BVR Editor). More results from BVR’s exclusive Firm Economics Survey. This installment looks at the marketing techniques that have been most effective at building the valuation practice.

- “Strong Pushback of Sec. 2704 Regs at IRS Hearing” (BVR Editor). An unprecedented number of speakers testified at the December 1 IRS hearing to fight the controversial proposed Section 2704 regulations designed to curb estate valuation discounts for minority interests

- “The 10 Most Important Valuation Cases of 2016” (BVR Editor). A roundup of the most impactful court cases that involve business valuation and the valuation of damages.

- “How to Better Validate the Reasons for Private-Company Discounts” (Anthony Carlton, Australia). This is a response to an article in the June 2016 issue of Business Valuation Update, in which Gilbert Matthews wrote about whether private companies are valued for less than public companies solely on the basis of being private or whether other factors are involved.

- “Main Lessons for Appraisers in the IPEV 2015 Valuation Guidelines” (Andrew Strickland, UK). The International Private Equity and Venture Capital 2015 Valuation Guidelines embrace a great many areas of business appraisal and provide guidance on some contentious areas.

- “Employee Equity Valuations: More Than Just a Black Box” (Jason Murphy, Australia). This first in a number of articles on valuing employee equity serves as an overview of the topic. In future issues, we will examine the various forms of employee equity and the methodologies and standards for their valuation.

The issue also includes:

- Regular features: “BV News At-a-Glance/Global Perspective,” “Ask the Experts,” and “Tip of the Month.”

- BV data spotlight: Pratt’s Stats MVIC/EBITDA Trends, ktMINE Royalty Rate Data, Economic Outlook for the Month, and Cost of Capital Center.

- BVLaw Case Update: The latest court cases that involve business valuation issues.

To stay current on business valuation, see the January issue of Business Valuation Update—now the eyes and ears of the BV profession around the globe.

back to top

BV movers

People: Keith Gordon has joined Boyer & Ritter of Carlisle, Pa., as a business valuation manager … Todd Harrington has been named managing partner of Lancaster, Pa.-based Trout Ebersole & Groff … Wes Nichols has joined Valuation Research Corporation as vice president in the firm’s Chicago office … Joshua Schroeder, a manager at Bauman Associates in Eau Claire, Wis., earned the CVA designation.

Firms: Charlotte, N.C.-based firms BGW CPA and Hawkins Conrad & Co. have combined and will continue in the Carolinas under the BGW name … Brixey & Meyer has acquired Cincinnati firm Kamphaus, Henning and Hood, whose employees will join B&M’s existing Cincinnati offices … Canfield, Ohio-based HBK has signed a merger agreement with Resnick, Amsterdam, Leshner of Blue Bell, Pa. … Ponte Vedra Beach, Fla.-based The Griggs Group has changed its name to Pivot CPAs … Prager Metis is merging with Long Island, N.Y.-based Cohen Greve & Co., effective January 1 … Weyrich, Cronin & Sorra, of Lutherville, Md., was named a “2016 Top Workplace” by The Baltimore Sun and WorkplaceDynamics LLC … Wipfli announced it is merging in Milwaukee-based firm Benes & Krueger, effective December 8.

Please send your professional and firm news to us at editor@bvresources.com.

back to top

Upcoming CPE events

Measuring Unjust Enrichment (December 14), with George Roach (George Roach Litigation Consulting). This is Part 7 of BVR's Special Series presented by The Comprehensive Guide to Economic Damages.

Down-to-Earth Considerations for Appraising Private Space Commercialization Companies (December 15), with Michael Blake (Arpeggio Advisors) and Stephen Fleming (Boostphase).

How to Measure Anything: Keynote Quarterly (January 12, 2017), with Douglas Hubbard.

Valuation of Small and Medium Sized Software Companies (January 19, 2017), with Hans Schroeder and Greg Carpenter.

Important note to webinar attendees: To ensure that you receive your dial-in instructions to BVR’s training events, please make sure to whitelist bvreducation@bvresources.com.

back to top

|

We welcome your feedback and comments. Contact Andy Dzamba (Executive Editor) or Sylvia Golden (Executive Legal Editor) at:

info@bvresources.com. |