|

|

BVWire is your go-to source for the latest in the business valuation profession. Highlights for this week include:

|

Solvency opinion based on management projections faces Daubert challenge

In a bankruptcy-cum-Daubert case that turned on solvency, a court recently rejected both parties’ claims that the opposing financial expert testimony was inadmissible. Among the myriad of attacks (all unsuccessful) against the experts was the plaintiff’s claim that the debtor’s expert had relied on management projections without scrutinizing the forecasts and examining the underlying facts or data. In contrast, the court found the expert’s deposition testimony, in particular, showed the expert assessed the reasonableness of the projections. Whether his decision to rely on the forecasts was reasonable was an issue for the jury to decide.

Failure to go behind the projections? The debtor was a pulp, paper, and tissue mill in Maine that suffered a business interruption loss and, in December 2013, received a cash settlement from its insurance company. Within six months, the board of directors authorized two distributions to a holding company that was the sole member of the debtor. Some 15 months after the last distribution, the debtor filed for Chapter 11 bankruptcy. The bankruptcy trustee appointed the official committee of unsecured creditors, i.e., the plaintiff in this case. The committee filed a lawsuit in which it tried to avoid and recover the distributions. The plaintiff argued the transfers were constructively fraudulent; the debtor was insolvent at the time of the distributions. In contrast, the debtor argued various solvency tests showed the debtor was solvent during the relevant times.

Both parties retained financial experts to support their positions, and both parties tried to exclude the rivaling expert under Federal Rule of Evidence 702 and Daubert.

The plaintiff criticized the defense expert’s solvency analysis under various tests: payment of debts test, balance sheet test, and capital adequacy test. According to the plaintiff, the expert testimony about the capital adequacy test and the income approach to the balance sheet test was unreliable, and, therefore, inadmissible, because the expert “blindly accepted mere summaries of management-prepared, EBITDA-level projections.” He did not test the reasonableness of the projections by examining the underlying facts or data or considering conflicting information, including other contemporaneous projections that were forecasting significant negative EBITDA. Also, if the expert had reviewed past financial performance against the then forecast performance, he “would have discovered that the Debtor’s prior performance was uniformly more negative than prior projections.”

‘Robust projection process’? The court found the plaintiff’s claim ignored evidence that the expert did question and analyze the reasonableness of the projections. For example, when asked during his deposition what he did to assess the reasonableness, he said he had reviewed deposition testimony of key board members and they all seemed to agree the projections included everything they knew at the time. According to the expert, the board members “talked to sales people, they talked to the operating people … So the projections were built from the ground up. It wasn’t somebody sitting in the office just making up numbers.” He said it appeared to him that the projection process was “fairly robust.” He also noted the board members “understood the business. They develop projections every year, budgets every year, reviewed financials.” He said he considered testimony from an outsider with industry expertise, who said the forecasts were reasonable. Moreover, he said, in the past, “they’ve hit $5 million of EBITDA or more.… So it’s not like they’re boldly going where no man has gone before.” Considering all of these factors “leads me to say that they’re reasonable.”

The court said the expert’s deposition testimony showed the expert (who was an accredited, experienced valuator) “applied his own expertise in assessing the reasonableness of the projections.” While the existence of opposing evidence may justify criticism of the expert’s conclusions, “that does not make his testimony inadmissible,” the court said. It added that the plaintiff could probe the reasonableness of the expert’s use of the projections through cross-examination, “and a jury can assess his response.”

The case is Official Committee of Unsecured Creditors v. Calpers Corp. Partners, LLC, 2020 U.S. Dist. LEXIS 125769 (July 17, 2020). Find a digest of all the valuation issues arising in the case and the court’s opinion at BVLaw (subscription required). |

|

Prospects grow for valuing promissory notes, says Mercer

There is an increasing number of opportunities for analysts in valuing promissory notes, says Chris Mercer (Mercer Capital) during the recent AICPA Forensic & Valuation Services Conference. As a result of many years of estate planning, there are “thousands and thousands of promissory notes out there” that are “coming of age,” he observes.

One method: Mercer was an expert in a 1996 estate tax case, Estate of Crosby, in which a U.S. District Court considered the valuation of a note held by an individual and payable by Champion International, a publicly traded company. The court rejected the valuation approach the IRS expert used and accepted the valuation by Mercer (at $3.6 million), whose analysis reflected greater detail in consideration of factors affecting the note. His method was to use the yield on Champion’s publicly traded debt as the “base” and then add to it based on the specific characteristics of the debt, much like adding company-specific risk to a discount rate. Mercer said he would be doing a white paper on this topic in the near future.

The full court opinion in the 1996 case, Estate of Verna Mae Crosby v. U.S.A., 77 AFTR2d Par. 96-541 (S.D. Miss 1996), is available at BVLaw.

Extra: Using publicly traded corporate debt as a proxy is not the only method for valuing small private promissory notes. See our coverage of an alternate method that the IRS is using.

|

|

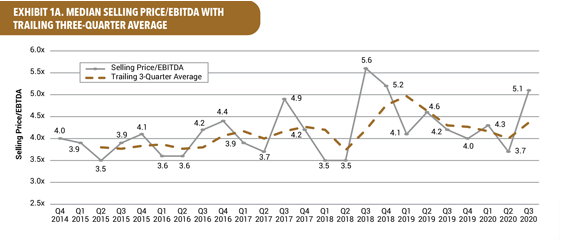

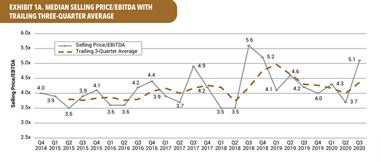

3Q20 private-company EBITDA multiples rise, per DealStats

After a drop in 2Q20, EBITDA multiples (median selling price/EBITDA) across all industries increased to 5.1x in the third quarter of 2020, the highest level since 2018, according to BVR’s DealStats Value Index (DVI) report. In 2Q20, the multiple had dropped to 3.7x as deal activity “nearly came to a standstill,” says the report. In addition, the trailing three-month average for multiples has increased in 3Q20 after dropping in the prior quarter (see graph). “As the economy, and in particular, the M&A transaction portion, continues to recover, DealStats will continue to monitor the trends in the EBITDA multiple,” says the report.

The DealStats Value Index (DVI) summarizes valuation multiples and profit margins for private companies that were sold over the past several quarters. The DVI is a quarterly newsletter and is complementary with a subscription to DealStats.

Extra: For transactions occurring during the pandemic, a little more investigation may be required as to why the deal took place. For example, bargain hunters may be looking for owners forced to sell. One idea: Call the broker--they’re named in the DealStats transactions and you can find their contact info from the Find an Intermediary database at https://data.bvresources.com/brokerfind.asp.

|

|

AICPA honors outstanding contributors to

FVS fields

During the 2020 AICPA Forensic and Valuation Services (FVS) Conference, a number of individuals were recognized for their contributions during the past year. Steven York, CPA, ABV, CEIV, CGMA, an executive vice president with Stern Brothers Valuation Advisors (Kansas City, Mo.), was named Business Valuation Volunteer of the Year. Peter Armstrong, CPA, CFF, a partner with KPMG LLP in Toronto, Canada, was named Forensic & Litigation Services (FLS) Volunteer of the Year.

The AICPA also released the 2020 list of Standing Ovation recipients. The Standing Ovation Program recognizes young CPAs holding the Certified in Financial Forensics (CFF) or Accredited in Business Valuation (ABV) specialty credentials who have exhibited exemplary personal achievement. The 2020 recipients are:

- Ashish Bagree, CPA, CFF (Arnie & Co. PC, Houston);

- Theodore Brown, CPA, CFF (Aprio LLP, Atlanta);

- Emily Chee, CPA, CFF, CITP (KPMG Canada, North Vancouver, British Columbia);

- Anne Cooper, CPA, ABV (StoneTurn, Houston);

- Mark DiMichael, CPA, ABV, CFF (Citrin Cooperman, New York City);

- Eric Flickinger, CPA, ABV (Apple Growth Partners, Akron, Ohio);

- Jesse Gillett, CPA, ABV, CFE (Edelstein & Co. LLP, Boston);

- Jordan Graves, CPA, ABV (Cooper Norman, Idaho Falls, Idaho);

- Nicholas Landera, CPA, CFF (Appelrouth Farah & Co., Coral Gables, Fla.);

- Andrew Leith, CPA, ABV, CFF (CBIZ MHM LLC, San Diego);

- William Lind, CPA, CFF (Hemming Morse LLP, Concord, Calif.);

- Ewelina Meczkowska, CPA, CFF, ABV (RSM US LLP, New York City);

- Stuart Neiberg, CPA, ABV, CFA (KapilaMukamal, Fort Lauderdale, Fla.);

- Monica Ospina, CPA, ABV, CFF (Forensic Accountants & Consultants PA, Tampa, Fla.);

- Hunter Outcalt, CPA, ABV (HealthCare Appraisers Inc., Boca Raton, Fla.);

- Micah Pycraft, CPA, CFF (Hemming Morse, Los Angeles);

- Kriste Rodriguez, CPA, ABV (EisnerAmper, Iselin, N.J.);

- Arielle Schmeck, CPA, ABV (J. Taylor & Associates LLC, Fort Worth, Texas);

- Anveshica Tayi, CPA, ABV (AlixPartners LLP, Dallas);

- Robert Taylor, CPA, CFF, JD, CVA (Taylor & Morgan, Flint, Mich.);

- Michelle Tran, CPA, CFF (Berkeley Research Group LLC, Houston); and

- Tyler Wright, CPA, ABV, CFF (Moore Colson CPAs and Advisors, Atlanta).

“These up and coming leaders in the forensic and valuation services arena are going the extra mile to advance the profession and serve their communities,” Barbara Andrews, director of forensics, technology, and management consulting for the AICPA, said in a statement. “Their efforts embody the spirit of volunteerism that the accounting profession is known for.” |

|

Tune in today for the ASA Virtual Fair

Value Conference

Leading-edge topics and nationally recognized speakers highlight the American Society of Appraisers Virtual Fair Value Conference being held today November 18. Sessions include a current issues panel, the impact of recent cases on the fair value of technology, an update on the working group developing The Appraisal Foundation’s valuation advisory on best practices in the application of company-specific risk premia, and much more. BVWire is attending the event, and we’ll provide coverage in future issues. Click here for more information. |

|

Home health and hospice sector bouncing back, per Levin study

Deal volume in the home health and hospice sector accelerated in the third quarter of 2020, up 120%, with 22 publicly announced transactions, compared with 10 acquisitions in the second quarter of 2020, according to data from HealthCareMandA.com and Deal Search Online. Compared with the same quarter in 2019, M&A activity increased by 10%. “Unlike most healthcare services sectors dealing with the coronavirus pandemic, home health care and hospice agencies are bouncing back to nearly pre-COVID-19 levels of activity,” says Lisa E. Phillips, editor of The Health Care M&A Report, which publishes the data. “Analysts we’ve talked to expected to see a resurgence of deals in the sector beginning in the third quarter, and they were right. There’s good momentum going into the fourth quarter, too.” The largest transaction in the third quarter was The Providence Service Corp.’s purchase of Simplura Health Group from One Equity Partners, for $575 million. |

|

IVSC solicits feedback on valuation topics

for agenda

The International Valuation Standards Council (IVSC), the global standard-setter for valuation practice and the valuation profession, has opened an Agenda Consultation to solicit input to help set the agenda for the future development of the International Valuation Standards (IVS). Feedback is wanted about valuation topics that the IVSC should address as part of its current agenda as well as additional valuation topics that should be prioritized or added to the agenda. Comments are due Jan. 15, 2021. To download the 2020 Agenda Consultation paper and how to submit feedback, click here. |

|

Preview of the December 2020 issue of Business Valuation Update

Here’s what you’ll see:

- “Little-Known Resource Can Help Bolster Support for Projections” (BVR Editor). Projections used in business valuation have always been subject to scrutiny—and now more than ever. During the recent ASA International Conference, it was pointed out that many valuation analysts may not know of a resource that can be used to help support their assessment of projections.

- “Can You Do Two Valuations With the Same Date? Yes, Says Hitchner” (BVR Editor). A valuation done pre-COVID-19 may be obsolete, so can you update it using the same valuation date and factor in the impacts of the pandemic? Yes, says James Hitchner (Valuation Products and Services), and he believes doing so is not in conflict with the valuation standards.

- “Several Trends of Note in Valuation Cases in the United Kingdom” (BVR Editor). A number of recent court cases in the UK are important to valuation. Matrimonial decisions continue to introduce valuation concepts beyond “fair value,” and, on the topic of goodwill, a recent case went contrary to the expectations of most business valuers.

The issue also includes:

- A full section of “BV News and Trends/Global BV News and Trends.”

- Regular features: “Ask the Experts” and “Tip of the Month.”

- BV data spotlight: “DealStats MVIC/EBITDA Trends,” “ktMINE Royalty Rate Data,” “Economic Outlook for the Month,” and the “Cost of Capital Center.”

- BVLaw Case Update: The latest court cases that involve business valuation issues.

To stay current on business valuation, check out the December 2020 issue of Business Valuation Update. |

|

BV movers . . .

People: Kevin Weckesser, CPA, CVA, will take over as president of Miamisburg, Ohio-based Brixey & Meyer Inc. effective Jan. 1, 2021; he is a 10-year veteran of the firm and leads the audit and assurance service line, in addition to providing advisory and business valuation services … Matt Stelzman, CVA, MAFF, ASA, has joined Windham Brannon (Atlanta) as a director in the firm’s forensics, litigation, and valuation practice; he has nearly 20 years of accounting firm experience and currently provides support in litigation matters by providing valuations for marital dissolution purposes and calculating lost earnings, lost profits, and economic damages … Andreas Barckow was appointed chair of the International Accounting Standards Board, effective July 2021, succeeding Hans Hoogervorst, who will complete his second five-year term in June 2021.

Firms: Savannah, Ga.-based Hancock Askew & Co. LLP is adding S. Mark Hand & Associates of Jacksonville, Fla., which specializes in tax, accounting, business valuations, and litigation support … Cincinnati-based Barnes Dennig & Co. Ltd. is adding Thorn Lewis + Duncan of Dayton, Ohio, a firm with 25 employees and in-depth experience in automobile dealerships and healthcare … Brea, Calif.-based Lance Soll & Lunghard LLP is adding Gray CPA Consulting of Montgomery, Texas, which specializes in custom financial report writing services … Baratz & Associates of Marlton, N.J., expands its footprint in southern New Jersey by adding Robin Kramer & Green of Fort Washington, Pa.; the combined firm will have 60 employees … To help strengthen its position in the architecture and engineering (AE) space, Stambaugh Ness of York, Pa., is adding accounting firm T. Wayne Owens & Associates of Augusta, Ga., and consulting firm TWO CPAs & Consultants of Dublin, Ohio … Shawano, Wis.-based KerberRose is adding Wolosek & Wolosek CPAs of Wisconsin Rapids, Wis.; the acquisition adds an 11th office location to KerberRose’s presence in northern Wisconsin … In Canada, Calgary-based MNP is adding Ville Saint-Laurent, Quebec-based firm KBHNS LLP, which provides accounting, tax, and advisory services to private enterprise companies in diverse industries throughout greater Montreal.

Please send your professional and firm news to us at editor@bvresources.com. |

|

CPE events

Learn why the underlying premise behind the size effect no longer holds and hear a review of the academic literature and empirical evidence on the absence of a size effect.

Learn about new research and available data you may need to consider when determining whether the COVID-19 pandemic is impacting company valuations because of changes in risk. |

Holiday Break

BVWire will be taking a break to enjoy the U.S. Thanksgiving holiday next week.

We will resume publication on Wednesday, December 2.

We wish you a very safe and happy holiday! |

|

We welcome your feedback and comments. Contact Andy Dzamba (Executive Editor) or Sylvia Golden, Esq. (Executive Legal Editor) at: info@bvresources.com.

|

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201

1-503-479-8200 | info@bvresources.com

© 2020. All rights reserved.

|

|