|

|

BVWire is your go-to source for the latest in the business valuation profession. Highlights for this week include:

|

ASA files amicus brief in Lee case, discussing FMV concerns in ESOP litigation

Responding to the appeal in the Lee case, the American Society of Appraisers recently filed an amicus brief supporting the dismissal of the case. The ASA draws attention to the fair market value (FMV) standard that applies in ESOP transactions and discusses the ESOP community’s longtime concern that the Department of Labor and some courts have all but abandoned FMV in scrutinizing ESOP transactions.

The Lee case arose out of the 2016 sale of shares in a construction company to an ESOP. The defendant trustee oversaw the transaction, and an experienced ESOP appraisal firm prepared the valuation underlying the transaction and subsequent annual valuations. The ESOP paid $198 million for an 80% ownership stake in the company. The transaction was financed with a loan from the company and the selling shareholders received warrants that would enable them to acquire additional voting stock. A 2016 year-end annual appraisal, which came 18 days later, valued the shares at $64.8 million.

The plaintiff’s complaint suggested that the two figures showed the trustee caused the ESOP to overpay for company stock. Last fall, a district court dismissed the case, finding the plaintiff had no standing as she failed to show she had suffered an injury. The plaintiff appealed the dismissal with the 4th Circuit Court of Appeals, and the Pension Rights Center (PRC), a nonprofit consumer organization, has filed an amicus brief supporting the appeal. The trustee has defended the dismissal of the case.

Not like a PE buyer: The ASA describes itself as the “largest multi-disciplinary organization devoted to the appraisal and valuation profession” whose members “regularly advise ESOP trustees on the FMV of employer stock for purposes of ESOP transactions, annual ESOP valuations, and other ERISA matters involving FMV appraisals.” Much of the ASA brief counters PRC’s argument that ESOP trustees should, but don’t, act like “real-world” buyers of companies, i.e., private-equity (PE) buyers. Some courts, too, “have been misled into error” on this issue, the ASA says. “Practices of PE buyers are incompatible with ERISA’s requirements and fundamental valuation principles,” the ASA brief contends.

No ERISA provision says a transaction is unlawful unless the ESOP trustee pursues the “lowest price possible for the ESOP” that a real-world (PE) buyer might pay, the ASA brief says. Rather, the valuation standard “specifically” required for ESOP transactions is the FMV. This is also the standard used for annual ESOP valuations, the brief notes. And it is the standard used in the Tax Code and regulations, in the Bankruptcy Code, and by a wide variety of statutes, the brief points out.

FMV is “not the lowest possible price a PE buyer might pay,” the ASA states. Instead, it is an “objective assessment of market forces, and it accounts for competing forces of sellers as well as buyers, both of whom seek to maximize gain.” PE buyers, the brief explains, don’t use the FMV standard for valuations. Rather, they look to “investment value,” a subjective estimate of what a specific buyer or group of investors might pay based on “subjective, personal parameters.” “PE valuations are guided by the rate of return an investor seeks,” the brief explains. In other words, a PE valuation does not consider the pressure “by a seller seeking the highest price.”

The ASA brief claims that, unlike a PE buyer, an “FMV appraiser adheres to valuation principles.” “The ESOP trustee’s statutory obligation to act in good faith does not require it to reject an FMV appraisal performed in accordance with valuation principles,” the brief says.

The ASA challenges a host of other claims about ESOPs that appear in the plaintiff’s and PRC’s briefs and “which are designed to color this Court’s views of ESOPs.” All of the claims are false, the ASA brief says. It notes that, in rejecting the plaintiff’s appeal, the 4th Circuit “has the opportunity to correct misimpressions that have been subjecting ESOPs to unjustified attacks.”

Stay tuned for further updates on this case.

A digest of the district court’s ruling in favor of the defendants in Lee v. Argent Trust Co., 2019 U.S. Dist. LEXIS 132066 (Aug. 7, 2019), and the court’s opinion are available to subscribers of BVLaw. Digests for Brundle v. Wilmington Trust N.A., 241 F. Supp. 3d 610 (E.D. Va. 2017); Brundle v. Wilmington Trust N.A., 258 F. Supp. 3d 647 (E.D. Va. 2017); and Brundle v. Wilmington Trust N.A., 919 F.3d 763 (4th Cir. 2019), and the courts’ opinions also are available at BVLaw. |

|

NCEO amicus brief supporting dismissal of case details benefits from ESOP participation

The National Center for Employee Ownership (NCEO) also filed an amicus brief in which it supports the dismissal of the Lee case that is currently on appeal with the 4th Circuit. NCEO says it seeks to “clarify[] what the available data show with respect to employee ownership so that the Court and its members can evaluate party litigation positions in the context of reliable information.”

The NCEO brief discusses the extensive academic research that has shown the advantages employees have received from participating in an ESOP plan, even in comparison with other retirement programs, such as 401(k) plans. The NCEO disputes the claim by the amicus curiae supporting the plaintiff, the Pension Rights Center (PRC), that ESOPs carry enormous risks for employees and are “vulnerable to abuse.” These are “unsubstantiated statements” that undermine the bipartisan Congressional efforts to encourage employee ownership, the NCEO says.

‘Conflating’ enterprise with equity value: According to the NCEO, the Lee plaintiff “mischaracterizes” the contested stock acquisition by “conflating enterprise value with equity value” when arguing the ESOP overpaid for company stock where the purchase price for the acquired stock was $198 million and a valuation that was done less than a month later valued the stock at $64.8 million.

“Where, as here, the ESOP uses debt financing to purchase company stock, the purchase price, which is based on the subject company’s enterprise value and capital structure prior to the transaction, is independent of the debt financing decision,” the NCEO explains. Adjusting for the debt would be inappropriate, the brief says. “Indeed … it would frustrate the fair market value standard that is generally applicable to ESOP stock purchase transactions.” No willing seller “not under any compulsion to sell” would agree to a lower purchase price to account for the debt burden to the buyer, the brief notes. In contrast, the equity value represents the value of the purchased equity less the transaction debt. In this case, the brief notes, the district court understood the difference, but the plaintiff did not. As happened in this transaction, “achieving an equity value greater than $0 within a short period of time after the transaction closing is an indicator that the purchase price was not only consistent with the fair market value standard, but also favorable to the buyer,” the NCEO brief says.

The NCEO brief accuses the plaintiff of attacking “the core concepts of ESOPs and ESOP stock purchase transactions.” Research has shown that ESOPs have been “strikingly successful” in enabling employees to build wealth, the NCEO says. DOL data show that ESOPs have “slightly” outperformed 401(k) plans in terms of rates of return and have had lower volatility. A 2017 research report sponsored by the DOL showed that, among workers sampled, those who participated in an ESOP had a 92% higher median household net wealth, 33% higher income from wages, and 53% longer median job tenure relative to workers who were not participants in an ESOP.

ESOPs consistently have received “Congressional blessing,” the NCEO brief says, as members of Congress have seen the data favoring employee ownership in companies.

The 4th Circuit Court of Appeals should “reject any negative presumption regarding ESOPs, should recognize what the figures alleged in the Complaint truly reflect about the prudence of the stock purchase transaction, and should affirm the judgment of the district court,” the NCEO brief says.

Stay tuned for further updates on this case.

A digest of the district court’s ruling in favor of the defendants in Lee v. Argent Trust Co., 2019 U.S. Dist. LEXIS 132066 (Aug. 7, 2019), and the court’s opinion, are available to subscribers of BVLaw. Digests for Brundle v. Wilmington Trust N.A., 241 F. Supp. 3d 610 (E.D. Va. 2017); Brundle v. Wilmington Trust N.A., 258 F. Supp. 3d 647 (E.D. Va. 2017); and Brundle v. Wilmington Trust N.A., 919 F.3d 763 (4th Cir. 2019), and the courts’ opinions also are available at BVLaw. |

|

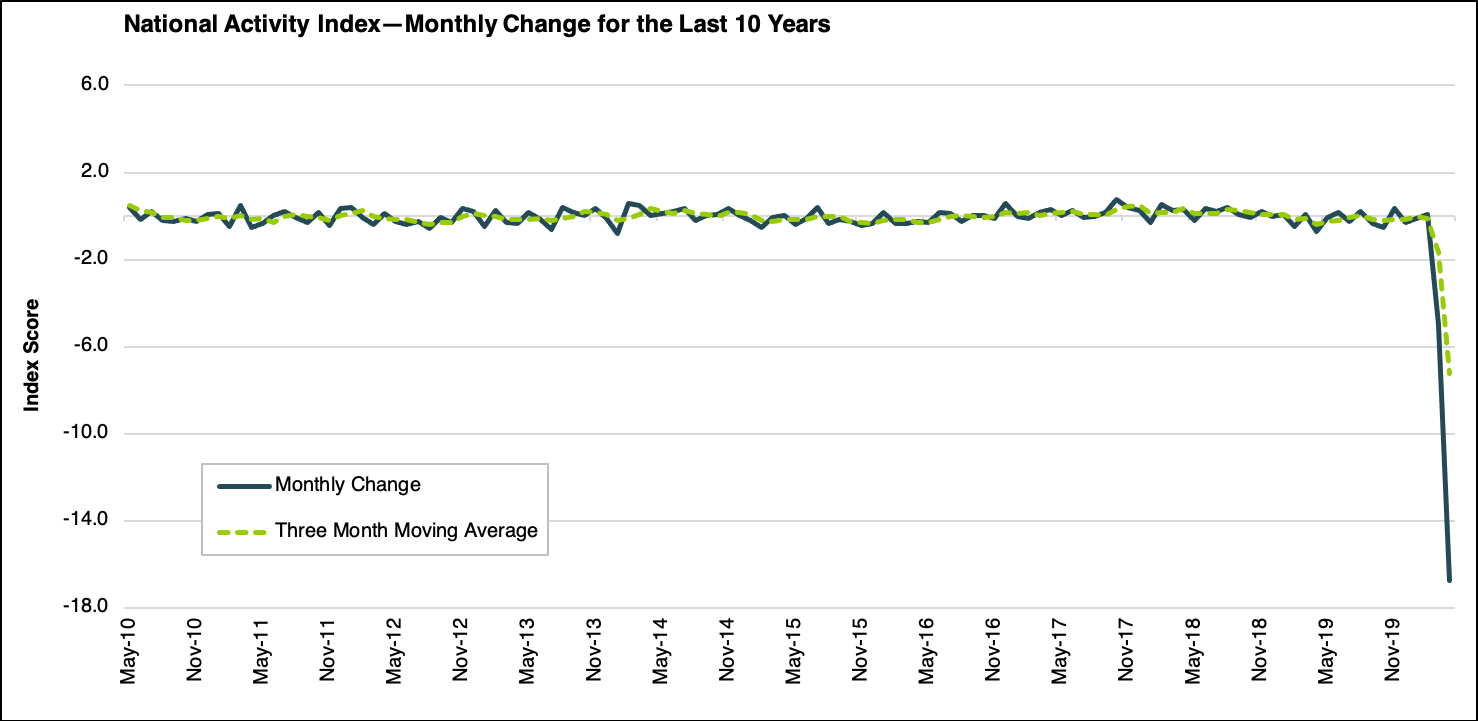

The CFNAI plunged to -16.74 in April

The Chicago Fed’s National Activity Index (CFNAI) came in at -16.74 in April, down from a revised -4.97 in March, as reported in the April 2020 issue of the Economic Outlook Update (see chart below). The April score, the lowest on record, fell as a result of the decline to 79 of the 85 individual indicators and to all four of the broad categories of indicators used to construct the index. All four categories decreased from their March levels as well. The index’s three-month moving average decreased to -7.22 in April, down from -1.69 in March. Following a period of economic expansion, an increasing likelihood of a recession has historically been associated with a three-month moving average value below -0.70.

Click to enlarge

The National Activity Index is designed to gauge overall economic activity and related inflationary pressure and includes 85 economic indicators that are drawn from four broad categories of data: production and income; employment, unemployment, and hours; personal consumption and housing; and sales, orders, and inventories. Each of these data series measures some aspect of overall macroeconomic activity. The derived index provides a single, summary measure of a factor common to these national economic data. In the history of the data series, the lowest score, 16.74, was recorded in April 2020 and the highest score, 2.07, was recorded in April 1978.

The April edition of the Economic Outlook Update also includes economic data that capture the full economic impact caused by the coronavirus lockdown. This includes the customary April data featuring the jobs and unemployment report, retail sales, housing market, and construction data but also added special reports from the University of Michigan and its Consumer Sentiment Survey, the U.S. Chamber of Commerce publishing its Small Business Coronavirus Impact Poll, the RSM Middle Market Business Index, White House Council of Economic Advisors, the PMI and NMI semiannual surveys, and the National Association of Realtors (NAR) Flash Survey, all of which provide an in-depth look at the economic damage caused by the coronavirus lockdown in their respective industries.

The 47-page April 2020 Economic Outlook Update contains expansive research from leading authoritative resources, which you can use in your valuation reports as long as you give proper attribution. To learn more, visit www.bvresources.com/eou. |

|

ASA Fair Value Virtual Conference airs live

June 18

Any practitioner involved in fair value should tune in to the first-ever ASA Fair Value Virtual Conference tomorrow, June 18. The American Society of Appraisers (ASA) has combined its New York and Los Angeles fair value events into one virtual conference that will cover a range of fair value measurement and valuation topics, as well as other current and future expected trends regarding the FASB, SEC, and international accounting standards. Highlights include a Big Four auditor’s panel, a discussion on the proposal to change the accounting for goodwill, and a report from a special task force on company-specific risk. Conference chairs are William A. Johnston (Empire Valuation) and Ray Rath (Globalview Advisors). |

|

Porter Award recipients announced at

NACVA confab

This week, BVWire is attending NACVA and the CTI’s 2020 Business Valuation and Financial Litigation Super Conference (online of course), where the recipients of this year’s Thomas R. Porter Lifetime Achievement Award have been named. Two individuals have received the award this year. First, Edward B. Cordes (posthumous), who formed the Denver-based Cordes Co. in 1983 and was very active with NACVA, serving and advising in various functions. In 2019, he established the Edward B. Cordes Scholarship Fund, which will fund over 30 full-ride scholarships for FFA students to attend a Colorado college or vocational school. The other recipient is Nancy Gault, a founding partner with CoNexus CPA Group (Atlanta), who has been very active with NACVA for many years, where she served as an ambassador and as NACVA’s Georgia State chapter president from 1996 to 2012.

The conference runs through this Friday, June 19. For those of you who can’t attend this week, the entire conference will be repeated the week of August 3-7 using the same virtual model and viewing options. |

|

D&P examines ‘breaking point’ for global firms

Almost half (47%) of alternative investment fund managers polled by Duff & Phelps say that three months is the “breaking point” at which the current economic restrictions impair the ability of businesses to resume business as usual after the lockdown. The survey received 118 respondents from North America (40%), UK (20%), and Europe (28%). Fund managers were predominantly invested in private equity (47%), private debt (15%), and venture capital (7%). The survey was conducted from April 3 to April 16. |

|

Preview of the July 2020 issue of Business Valuation Update Here’s what you’ll see:

- “Tales From the Trenches: Think Twice About Adding M&A Services to Your BV Practice” (Robert E. Kleeman Jr., CPA/ABV, ASA, OnPointe Financial Valuation Group LLC). Expanding into M&A services might appear to be a great growth area for your existing business valuation practice; however, the author believes that this strategy may be fraught with danger and may do more harm to your existing practice than help to grow it.

The issue also includes:

- An expanded section of “BV News and Trends/Global BV News and Trends.”

- Regular features: “Ask the Experts” and “Tip of the Month.”

- BV data spotlight: “DealStats MVIC/EBITDA Trends,” “Stout Restricted Stock Study and DLOM Calculator,” “Economic Outlook for the Month,” and the “Cost of Capital Center.”

- BVLaw Case Update: The latest court cases that involve business valuation issues.

To stay current on business valuation, check out the July 2020 issue of Business Valuation Update. |

|

BV movers . . .

People: Audra M. Moncur, CPA, ABV, and Paul D. Ouweneel, CFA, CPA, CFP, have been promoted to partner at Milwaukee-based Wipfli; Moncur leads the valuation services group in Illinois, and Ouweneel is in the valuation, forensic, and litigation services practice in the firm’s Milwaukee office … Lim Hwee Hua, former Cabinet Minister in the Government of Singapore, has joined the board of directors of the International Valuation Standards Council.

Firms: New York City-based Prager Metis has acquired William J. Keephart CPA of Lawrenceville, N.J. … BKD CPAs & Advisors has launched a new transfer pricing services division in the firm’s Salt Lake City office … Pivot CPAs of Ponte Vedra, Fla., has opened a new office in Gainesville, also in northeast Florida … Hilco Global and New York City-based Colbeck Capital Management have acquired the assets of the transportation and truck leasing company, 19th Capital, headquartered in Indianapolis.

Please send your professional and firm news to us at editor@bvresources.com. |

|

CPE events

Perhaps no industry has been impacted more by COVID-19 than the healthcare industry. Four top healthcare valuation and finance experts share their insights.

Identifying and linking balance sheet financials to company-specific risk is a critical skill for valuation professionals to master—especially during the current pandemic.

|

|

We welcome your feedback and comments. Contact Andy Dzamba (Executive Editor) or Sylvia Golden, Esq. (Executive Legal Editor) at: info@bvresources.com.

|

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201

1-503-479-8200 | info@bvresources.com

© 2019. All rights reserved.

|

|