How the far-reaching new lease accounting rules will impact financials

Ten years in the making, the International Accounting Standards Board has issued a final standard (IFRS 16, Leases) that will require companies to bring leases onto the balance sheet. The new standard, effective Jan. 1, 2019, replaces the current guidance in IAS 17. IFRS 16 and the soon-to-be published guidance from the Financial Accounting Standards Board (FASB) under U.S. GAAP are not expected to be fully converged.

Primary effects: The rules will thrust about $2.5 trillion onto the balance sheets of listed companies using IFRS or U.S. GAAP. These companies will also show higher operating profits. Total cash flows would be unaffected, but you will see an increase in the amount of operating cash and a decrease of financing cash, according to the IASB.

Accompanying its new standard, the IASB has also published a separate effects analysis document. Last year, the IASB put out a similar document that also compares the IASB’s requirements to those of the FASB.

Video debrief: In a YouTube video, IASB chairman Hans Hoogervorst explains the new standard, which will “provide much-needed transparency on companies’ lease assets and liabilities, meaning that off balance sheet lease financing is no longer lurking in the shadows,” he says. “It will also improve comparability between companies that lease and those that borrow to buy.”

back to top

DLOM ruling promises end to ‘most difficult case’

Third time’s a charm? A nasty shareholder dispute that has lasted for two decades and featured rock-star valuators recently prompted a third appeals court ruling related to the marketability discount.

Case for DLOM: A sister and two brothers owned equal shares in a family trucking business. In 1996, one brother filed an oppressed shareholder action claiming his siblings tried to oust him from the company. The trial court found that the plaintiff brother in fact was the oppressing shareholder and ordered him to sell his interest either to the company or to the two siblings at fair value.

Both parties retained well-known appraisers. When the first trial court set a value without conducting an evidentiary hearing, the parties appealed. On remand, a different trial court heard valuation testimony and largely adopted the calculation the plaintiff’s expert proposed. It was based on a discounted cash flow (DCF) analysis. A second appeal followed. The appeals court affirmed nearly all aspects of the trial court’s value findings but said the valuation should have included a marketability discount.

Although a marketability discount was only applicable under “extraordinary circumstances” in a forced buyout situation, it was justifiable here because the plaintiff-seller had engaged in conduct that harmed the two other shareholders (defendants) and necessitated the forced buyout. Accordingly, the appeals court remanded again, ordering the trial court to determine whether the prevailing DCF analysis embedded a DLOM and set the applicable DLOM rate.

On the low end of spectrum: A third trial judge (two trial court judges had retired during the litigation) first found that, when the prevailing expert built up his discount rate for the DCF analysis, he did not specifically account for illiquidity. In the valuation trial, he had insisted a marketability discount was inappropriate because the company was successful and would likely take no longer to sell than other closely held companies of similar size and nature with assistance from “the right business intermediary.” He also believed the other shareholders would not lose liquidity during the marketing period.

As for the appropriate discount rate, the new trial judge noted that the buyers’ expert had valued the company under a market approach and had considered risk factors specific to liquidity—which were pretty much the same factors the opposing expert considered for his discount rate—to arrive at a 35% DLOM. A rate that high would unduly punish the seller and give a significant windfall to the buying shareholders, the trial court said. Case law and studies suggested a broader range, starting as low as 20%, depending on the equities in a given case. Here, a 25% DLOM was appropriate.

The parties appealed anew, but the reviewing court affirmed. It said that neither side had made a convincing argument for second-guessing the trial court’s “thoughtful and well-reasoned determination in this most difficult case.”

Takeaway: In building up the discount rate underlying his DCF analysis, the prevailing expert did not specifically adjust for lack of marketability (illiquidity). Therefore, an independent 25% DLOM was applicable to the valuation.

Find an extended discussion of Wisniewski v. Walsh, 2015 N.J. Super. Unpub. LEXIS 3001 (Dec. 24, 2015) (Wisniewski II), in the March edition of Business Valuation Update; the court’s opinion will be available soon at BVLaw. A digest of the prior appeals court decision, Wisniewski v. Walsh, 2013 N.J. Super. Unpub. LEXIS 724, is also available at BVLaw.

back to top

When to consult a compensation expert

Sometimes, the valuation analyst can establish reasonable compensation. Other times, you need to call in a compensation consultant.

First question: The first issue to look at is the potential impact of a compensation adjustment. “You need to determine if an adjustment will have a material impact on the value conclusion or the outcome of the particular matter,” says Mark Higgins, president of Higgins, Marcus & Lovett, a business valuation and litigation consulting firm based in Los Angeles. He points out that an adjustment will have a different impact depending on the size of the subject company and the magnitude of the potential adjustment.

Once the above issue—and others—are addressed, the decision to bring in a compensation expert will depend on the level of review and analysis that will be required. Higgins lays out the thought process he uses in deciding when to call in extra help in an article in the February issue of Business Valuation Update.

back to top

New research on financial-sector cost of capital

A new paper has been posted on the website of the Social Science Research Network (SSRN): “The Cost of Capital of the Financial Sector,” by Tobias Adrian (Federal Reserve Bank of New York), Evan Friedman (Columbia University), and Tyler Muir (Yale University). The authors propose a five-factor asset pricing model that complements the standard Fama and French three-factor model with a financial sector ROE factor (FROE) and the spread between the financial sector and the market return.

back to top

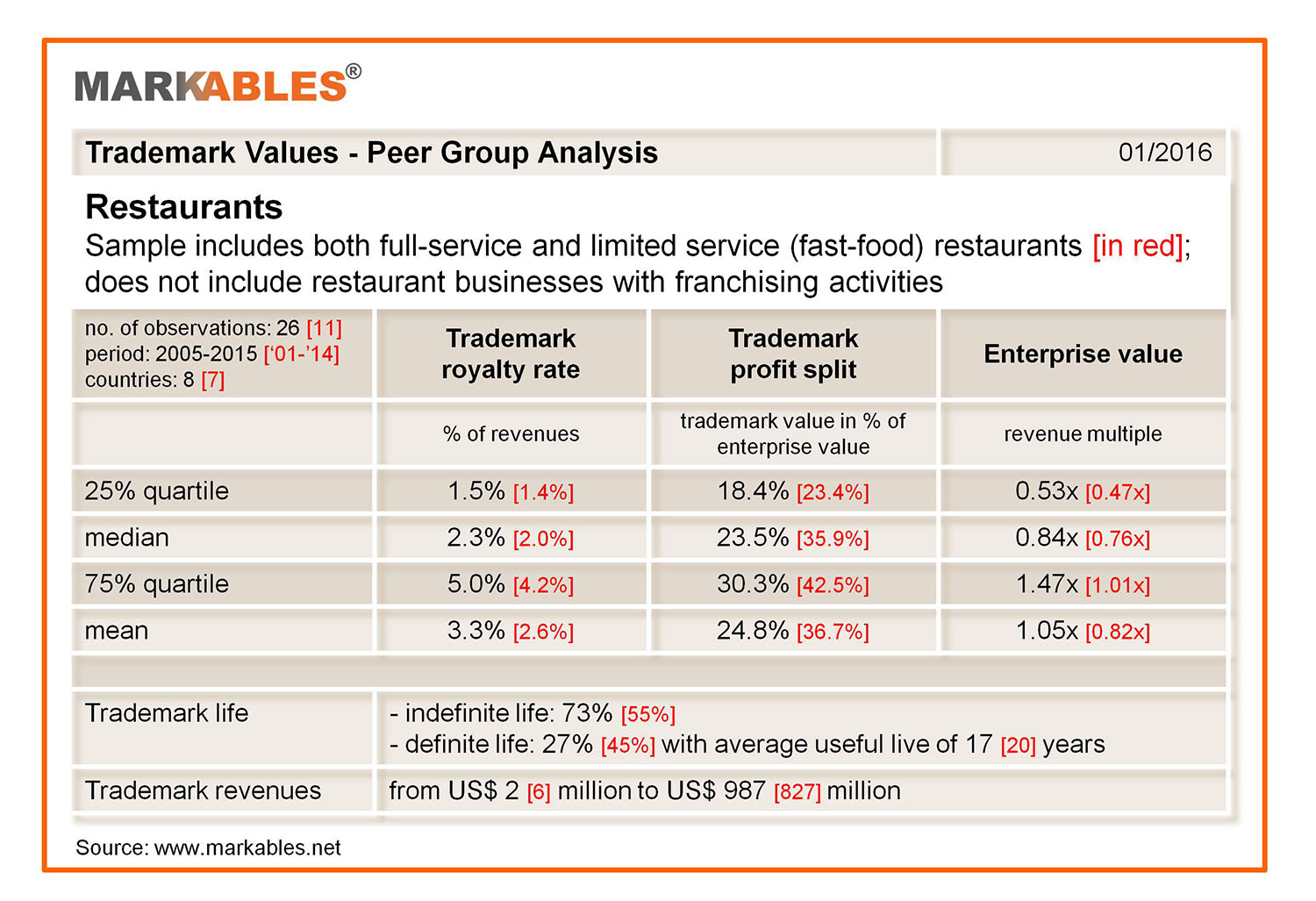

Restaurant brand value multiples keyed to price positioning

When eating out, how important is the restaurant brand? An analysis from Markables illustrates trademark comparable data for both full service and fast food restaurants (fully owned and operated restaurants only, not franchised operations). Some of the larger restaurant brands in the sample are LongHorn Steakhouse, The Capital Grille, O’Charley’s, Yard House, Roman’s Macaroni Grill, Mimi’s Café, and Einstein Bros. Bagels, among others.

Two key points: The analysis reveals two noteworthy issues. First, restaurant brand value multiples depend on the price positioning of a particular brand. Full service, sit-down restaurants generate a higher brand value premium than fast food restaurants. The same observation can be made within each group. Second, pure play trademark royalty rates must not be confounded with franchise royalty rates, which are most often in the area of 4% to 6% on revenues. As a rule of thumb, the value of the trademark makes up for approximately 50% of the franchise, with the remainder for the operating system, recipes, and trade secrets.

Trademark royalty rates range from 1.5% to 5% on revenues, with median rates of 2.3% for full service and 2.0% for fast food restaurants (see chart). The trademark accounts for about 25% of enterprise value of full service restaurants and 35% for fast food restaurants. Average enterprise value multiples for the sector are 0.85x revenues for full service and 0.75x for fast food restaurants.

Markables, based in Switzerland, has a database of over 6,500 trademark valuations published in financial reporting documents of listed companies from all over the world. The database reports value solely for the use of trademarks (not bundled with other rights).

Click on image to view full size.

back to top

Valuation multiples in healthcare services

The S&P Healthcare Services Index increased 2.6% over the last three months, performing worse than the S&P 500, which increased 4.6% over the same period, according to the December 2015 Healthcare Sector Update from Duff & Phelps. The best-performing sectors were specialty managed care (up 19.0%), assisted/independent living (up 6.2%), and home care/hospice (up 4.7%). The worst-performing sectors were acute care hospitals (down 23.4%), skilled nursing (down 16.8%), and diagnostic imaging (down 12.7%)

The current median LTM revenue and LTM EBITDA multiples for the healthcare services industry overall are 1.51x and 12.4x, respectively. The sectors with the highest valuation multiples include: healthcare REITs (12.0x LTM revenue, 17.9x LTM EBITDA); psychiatric hospitals (0.3x LTM revenue, 20.3x LTM EBITDA); HCIT (3.6x LTM revenue, 17.7x LTM EBITDA); and emergency services (2.7x LTM revenue, 18.1x LTM EBITDA).

back to top

Global BV news:

Of valuation and plum brandy in Serbia

If you’re ever in Serbia, try the brandy made from some of the best plums in the world, according to Danijela llic and Vesna Stefanovic of the National Association of Valuers of Serbia (NAVS), the newest member VPO of the International Institute of Business Valuers (iiBV). In an interview, they talk about valuation in Serbia, including the sources of data they use, which include historical financial statements and business projections as well as Bloomberg, InFinancial, and Euronext. As for the stock exchanges as data sources, they say that the Serbian stock exchange BELEX is illiquid, so valuation analysts look to global databases, such as Deutsche Börse and the London Stock Exchange.

They also mention that business valuation used to be highly regulated for privatization of state and socially owned companies, and valuations were done using adjusted book value, DCF, and liquidation value. These methods are still being used, although many CFAs are using EBITDA techniques, although there are issues with market data transparency and illiquid markets.

back to top

|

Review of book that proposes new PTE valuation model

A review of the book Taxes and Value: The Ongoing Research and Analysis Relating to the S Corporation Valuation Puzzle is in the latest edition of NACVA’s QuickRead. The book, written by Nancy J. Fannon (Meyers, Harrison & Pia LLC) and Keith Sellers (University of Denver), presents research that challenges the pass-through entity valuation models used by the Tax Court and the IRS, and it proposes a new model for valuing these entities.

Good timing: The reviewer, Roberto Castro, Esq. (WealthCounsel; Central Washington Appraisal, Forensics and Economics LLC), writes: “Given that it is the beginning of the year, that S corporation shareholders may be discussing exit strategies and buy-sell agreements, and that many valuation analysts provide consulting services too, perhaps it is worth considering what Fannon and Sellers have to say about valuing S corporations.”

For more information on the book, click here.

back to top

BV movers . . .

People: Elizabeth Cordaro has been appointed director of the healthcare practice at Ankura Consulting Group and will work out of the firm’s Dallas office … Steven Egna has joined the team at Valuation Resource Group and will be based out of New York City … Former IRS litigator, Jon Feldhammer, who specializes in the valuation of assets in estate and gift taxes, has joined Schiff Hardin’s San Francisco office as partner in the general corporate and securities group … Robert Hilton has joined Katz, Sapper & Miller as director in its Valuation and ESOP Services groups, further cementing the firm's deep commitment to its rapidly growing and geographically diverse client base. Rob will be based in Rochester, N.Y.

Firms: The national firm Doeren Mayhew has acquired Adler & Co., a CPA firm based in Farmington Hills, Mich., which has provided accounting and tax services to small businesses and high-net-worth individuals in the metro Detroit area for over 30 years … Duff & Phelps was ranked No. 1 for the number of fairness opinions rendered in the U.S. and tied for first in the number of fairness opinions rendered globally by Thomson Reuters’ annual report, 2015 Mergers & Acquisitions Review … With eyes on expansion into the New York City market, the New York firms Gettry Marcus and MLGW merged on January 1 and will operate under the Gettry Marcus brand … For the third consecutive year, INSIDE Public Accounting ranked GBQ’s Valuation & Financial Opinions practice as the “No. 1 Valuation Practice” as measured by valuation volume relative to total firm revenues nationally … HLB International, a global accountancy organization, has added three new members in Lisbon, Portugal: Conceito SA, APPM & Associado, and Victor Jose & Associados, creating one of the largest accounting networks in Portugal … HORNE LLP, a national CPA and business advisory firm, acquired the Mississippi-based cybersecurity firm, Halberd Group, and has established HORNE Cyber Solutions, a division whose focus is on IT services in the areas of cybersecurity, strategic advisory, ERP services, regulatory compliance, and IT assurance.

back to top

CPE events

Valuing Midstream Oil and Gas Companies (January 27), with Tom Ramos (BDO Consulting) and Dan Visich (BDO Consulting).

Alternative Energy-Understanding Critical Business Valuation Issues (February 11), with Rick Daubenspeck (BDO Consulting) and Donna Lobete (BDO Consulting).

Measuring the Discount for Lack of Marketability for Restriction Periods of Any Length (February 16), with John Finnerty (Finnerty Economic Consulting LLC).

Valuing Specialty Paving Contractors (February 18), with Brad Minor (Blue).

Important note to webinar attendees: To ensure that you receive your dial-in instructions to BVR’s training events, please make sure to whitelist bvreducation@bvresources.com.

back to top

|

We welcome your feedback and comments. Contact the editor, Andy Dzamba at:

info@bvresources.com or (503) 291-7963 ext. 133 |